If you got a job offer recently or are in discussion for your compensation package, knowing what 4.5 LPA in hand salary really means is the first thing to know before you sign on that dotted line! CTC (Cost to Company) is often confused between freshers and mid-level professionals in India, with take-home pay, but the difference can be considerable. This detailed guide takes you through every part of a 4.5 LPA salary – gross pay, net in-hand amount, taxes, and deductions – along with tips to get the maximum from what you receive.

What Does 4.5 LPA Mean?

LPA = Lakhs Per Annum, which is a standard method for quoting annual salary packages in India. For example: 4.5 LPA = ₹4,50,000 per year ← CTC, but CTC is not to be confused with what you earn as salary credited in your bank account every month. CTC is a collection of your basic salary, allowances, employer’s contribution toward Provident Fund (PF), gratuity, insurance premiums and other benefits, much of which you never receive as cash in hand.

You might be well versed with your CTC (Cost To Company), but to know by how much you would gain in hand each month, it is important to know your actual 4.5 LPA in hand salary too, which can be derived by considering all compulsory/ mandatory deductions and non-cash components as well from the CTC.

Monthly Gross Salary at 4.5 LPA

Starting with the gross monthly number, before making any deductions

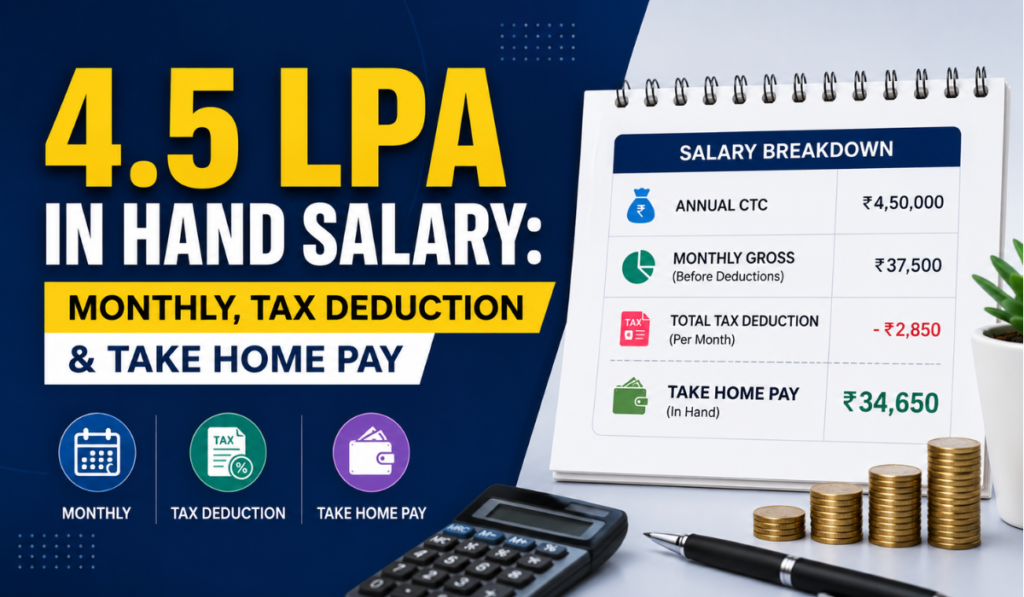

- Gross Monthly = Annual CTC ÷ 12

- Gross – ₹4,50,000 ÷ 12 = ₹37,500 (per month)

- Your gross monthly salary meaning before tax. The actual in-hand or net salary you get is less.

Read Also: 6 LPA In Hand Salary: Monthly Income, Deductions

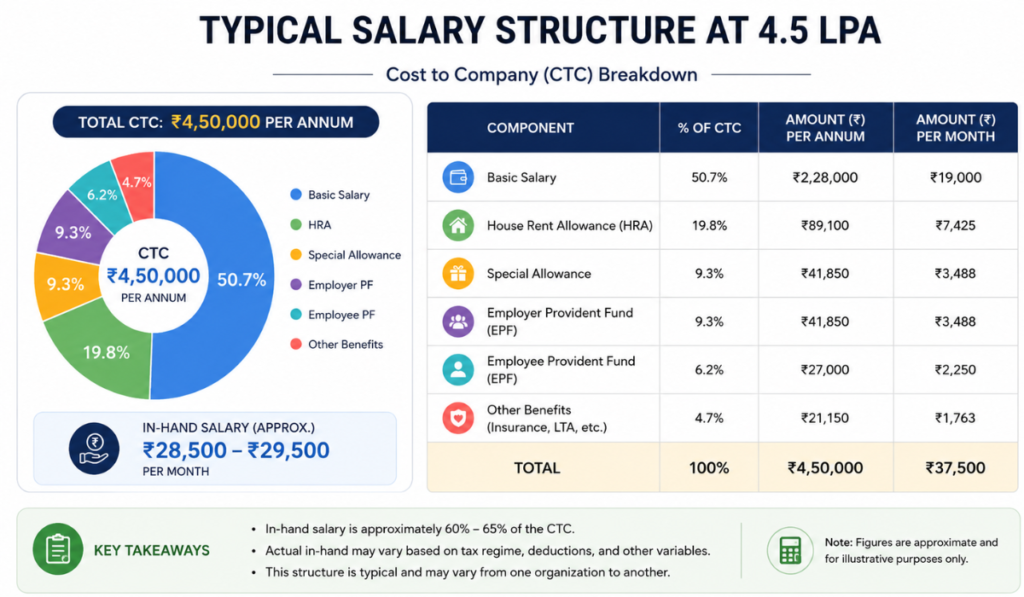

Typical Salary Structure at 4.5 LPA

That is the norm among Indian companies that structure their salary packages with multiple components. A typical distribution of a 4.5 LPA package would look something like this:

| Salary Component | Annual Amount (₹) | Monthly Amount (₹) |

| Basic Salary (40–50% of CTC) | 1,80,000 | 15,000 |

| House Rent Allowance (HRA) | 90,000 | 7,500 |

| Special Allowance | 90,000 | 7,500 |

| Leave Travel Allowance (LTA) | 18,000 | 1,500 |

| Medical Allowance | 15,000 | 1,250 |

| Employer PF Contribution | 21,600 | 1,800 |

| Gratuity (4.81% of Basic) | 8,658 | 721 |

| Total CTC | 4,23,258 | 35,271 |

Important Info: Exact structures may vary from employer to employer. Certain companies add the performance bonuses, meal allowances or transport allowances to the CTC that lower your fixed monthly pay.

Understanding Deductions at 4.5 LPA

There are two types of deductions (from your gross salary): statutory deductions (as per law) and voluntary deductions (which are selected by the employee).

Statutory Deductions

Employee Provident Fund (EPF) The Employee Provident Fund is a monthly contribution with both the employer and employee contributing 12% of the basic salary each month towards this retirement savings scheme.

- Deduction of Employee EPF Contribution = 12% of Basic which is ₹1,800/month

- EPF contribution by Employer = ₹1,800/month (this is part of CTC; not deducted from gross)

Professional Tax (PT) Professional tax applies to salaried individuals and is imposed by state governments, which means it varies depending on the state you live in. It varies from ₹150 to ₹200 per month in this wage bracket in most states. Here in this article, we will take ₹200/month for example.

49 for the financial year 2021-22 The income on which TDS Is deducted Income Tax (TDS) If your net taxable income is less than Rs.4.5 LPA then due to the basic exemption limit under section 80C this condition may be applicable while filing ITR2 along with Deductions Under Section 80D, the state/UT in which you live may have been set to “Do Not Share” by default so check carefully as else both these states will appear only once after it. New Tax Regime Applicable (2024–25):

- Income up to ₹3,00,000: Nil

- ₹3,00,001 to ₹7,00,000: 5%

In the case of the New Tax Regime (if you claim ₹75,000 as standard deduction), it will become your taxable income:

For example, salaried persons have to pay under the new tax slabs as follows: Income of ₹4,50,000 − ₹75,000 (standard deduction) = 3,75,000

Tax on ₹3,75,000 = 5% on (₹3,75,000 − ₹3,00,000) = 5% × ₹75,000 = ₹3.750/py = ₹312.50/pem

But section 87A provides a rebate on income up to ₹ 7 lakhs, and the amount is up to ₹25000. What this means is your tax outgo on income up to ₹7 lakhs after standard deduction becomes Nil.

4.5 LPA In Hand Salary: Monthly Calculation

Below is a clear, precise in-hand salary calculation for the 4.5 LPA In Hand Salary, assuming standard deduction and nil income tax:

| Particulars | Monthly Amount (₹) |

| Gross Monthly Salary | 37,500 |

| Less: Employee PF (12% of Basic) | −1,800 |

| Less: Professional Tax | −200 |

| Less: Income Tax (TDS) | 0 (rebate under Sec 87A) |

| In-Hand Monthly Salary | 35,500 |

- Approximate in-hand salary at 4.5 LPA = ₹35,000 to ₹36,000/month.

This number does not take into account any extra deductions such as employee insurance premiums, NPS deduction or salary advance repayment. With ESI (Employees’ State Insurance this is applicable if your gross salary comes below ₹21,000/month. Add another 0.75% deduction if your company deducts it from your paycheck.

Read Also: 7 LPA In Hand Salary: Monthly Salary, Deductions & Take Home Pay

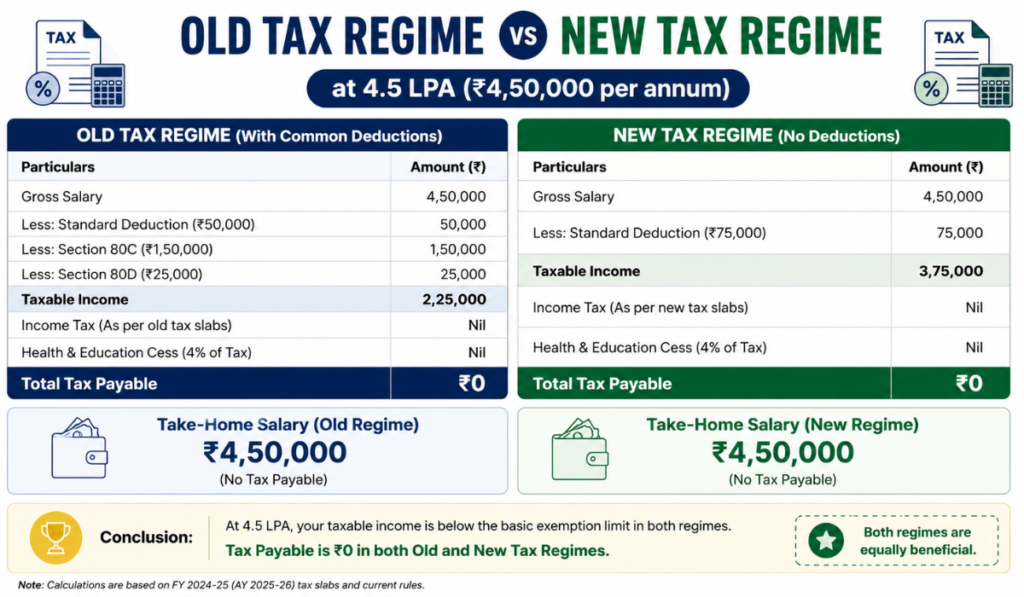

Old Tax Regime vs New Tax Regime at 4.5 LPA

Your in-hand salary will be impacted by the tax regime chosen. Here’s a comparison:

| Tax Parameter | Old Tax Regime | New Tax Regime |

| Standard Deduction | ₹50,000 | ₹75,000 |

| Section 80C Deduction | Up to ₹1,50,000 | Not available |

| HRA Exemption | Available | Not available |

| Taxable Income (after deductions) | Potentially ₹0–₹1,00,000 | ₹3,75,000 |

| Income Tax Payable | Nil | Nil (rebate Sec 87A) |

| Best For | Those with high 80C investments & HRA claims | Simplicity with fewer investments |

At4.5 LPA In Hand Salary and below, income tax is NIL for almost all employees under both regimes due to standard deductions and section 870 rebate. But if your 80C investments are high and your rent too, the old regime can save you little more.

How Employer PF Contribution Affects Your CTC

Employer PF contribution is one of the most misinterpreted parts of CTC. Most job offerings cover the 12% PF contribution (₹1,800/month or ₹21,600/year) of the employer in the CTC figure. That figure is never deposited directly into your bank account; it finds its way to one of your EPF accounts as a long-term savings bucket.

Now, if you have an offer letter of ₹4.5 LPA with employer PF, then your gross salary will be on the following basis:

- CTC actual Gross (₹4,50,000 − ₹21,600 (Employer PF) − ₹8,658(Gratuity))= ₹4,19,742

- That just translates to ₹34,978/month gross, approximately ₹33,000/month in hand (after employee PF+professional tax.

- This is the reason why you need to ask your HR if the CTC includes or excludes employer PF and gratuity.

4.5 LPA In Hand Salary: City-Wise Perspective

The other big part is, your in-hand salary is more or less the same across all cities (tax laws are central), but purchasing power and cost of living vary significantly. Check out how ₹35,000/month stacks up in some Indian cities:

| City | Avg. Rent (1BHK) | Monthly Expenses (approx.) | Savings Potential |

| Tier-1 (Mumbai, Delhi) | ₹18,000–₹25,000 | ₹30,000–₹35,000 | Very Low |

| Tier-1 (Bengaluru, Pune) | ₹12,000–₹18,000 | ₹25,000–₹30,000 | Low to Moderate |

| Tier-2 (Jaipur, Lucknow) | ₹6,000–₹10,000 | ₹18,000–₹22,000 | Moderate to High |

| Tier-3 / Hometown | ₹3,000–₹6,000 | ₹12,000–₹16,000 | High |

Mumbai and Delhi, at 4.5 LPA In Hand Salary, are somewhat tight when living independently in these cities. But this salary provides you with a comfortable living with good ability to save in Tier-2 and Tier-3 cities.

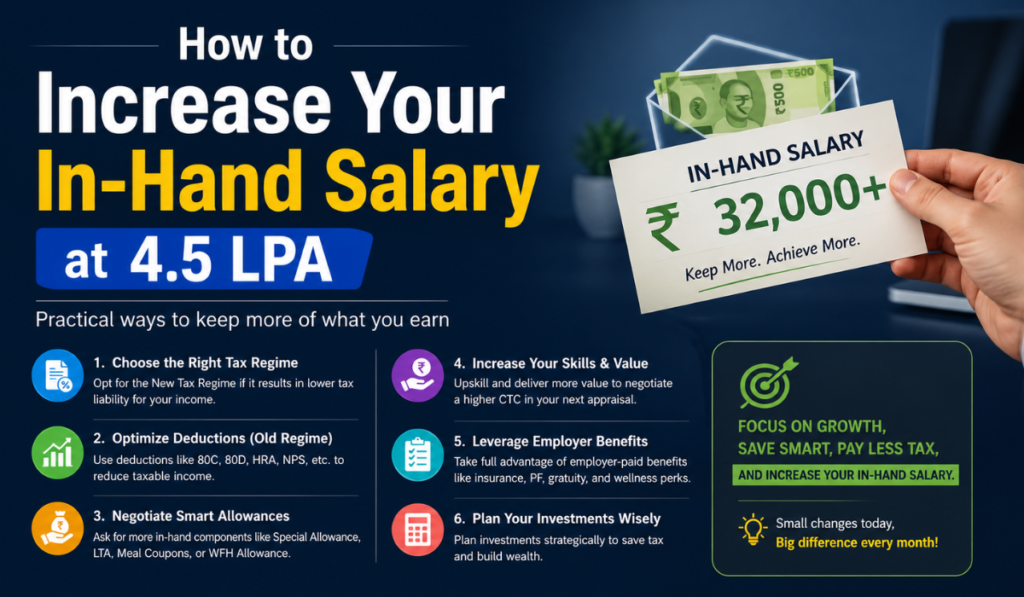

How to Increase Your In-Hand Salary at 4.5 LPA

While your CTC is fixed, it is possible to argue for higher take-home pay in just and proper manners.

- Claim HRA Exemption (Old Regime)

If you are a rent payer, declare HRA exemption u/s 10(13A) in the old tax regime. Reduce taxable income substantially.

- Maximise Section 80C (Old Regime)

Deduction is available for investment up to ₹1.5 lakh in PPF, ELSS MF, EPF, NSC or life insurance premium. This can decrease taxable income down to almost zero at 4.5 LPA using the old regime.

- Optimise Salary Structure with HR

Request your employer to re-align your CTC with more tax-exempt components by adding allowances like:

Leave Travel Allowance (LTA) is exempt for two journeys in a 4-year slab. In terms of Food Coupons / Meal Allowances, Band / Student A may receive otherwise tax-exempt allowances (up to ₹2,200/month). Phone & Internet Reimbursement actual expenses can be tax-exempt

- Choose the Right Tax Regime

Do a quick calculation every year. All taxpayers offer zero tax at 4.5 LPA under either regime, but with investments, the post-tax outcomes on a higher gross salary may still favour the old regime, as well as lower taxable salaries.

- Do Not Exceed The Mandatory Limit For Voluntary PF

Voluntary PES contributions decrease your take-home pay. Unless you plan to change careers or retire, save the required 12% as it gives you more monthly cash.

Read Also: 2 LPA In Hand Salary: Monthly Salary, Deductions

Annual vs Monthly Break-up Summary

Here is a full reference chart of annual and monthly salaries:

| Component | Annual (₹) | Monthly (₹) |

| CTC | 4,50,000 | 37,500 |

| Gross Salary (excl. employer PF & gratuity) | 4,19,742 | 34,978 |

| Employee PF Deduction | 21,600 | 1,800 |

| Professional Tax | 2,400 | 200 |

| Income Tax (TDS) | 0 | 0 |

| Net In-Hand Salary | ~3,95,742 | ~32,978–35,500 |

This is because CTCs are all structured differently, which leads to different amounts of cash in hand. Insist on a break-up offer letter at all times.

Is 4.5 LPA a Good Salary in India?

4.5 LPA In Hand Salary is a good salary or not depends on several factors:

For Freshers: 4.5 LPA is well above the fresher average salary in India (which lies around ₹3–4 LPA). So this is a good starting point, more so if you belong to Tier-2 cities or your living expenses are not much.

Experienced Professionals (3–5 years): 4.5 LPA is on the lower side, depending on your domain. And by this point, professionals in IT, finance or consulting are making ₹6–12 LPA. Consider negotiating or acquiring additional skills.

For Remote Workers / Freelancers: The effective purchasing power for remote workers and freelancers earning 4.5 LPA is significantly higher than that of a metropolitan-based employee making the same amount as well

Frequently Asked Questions (FAQ): 4.5 LPA In Hand Salary

Q1. How much is the in-hand salary of 4.5 LPA?

The in-hand salary of a package of 4.5 LPA will be between ₹32k and ₹36k per month, depending upon CTC structure, employer PF policy, professional tax and any other additional deductions made. If you are at standard structures, expect an in-hand of ₹ 35,000 / month approximately.

Q2. Income tax on 4.5 LPA in most cases, no income tax is payable on 4.5 LPA.

The new tax regime’s standard deduction of ₹75,000 falls above ₹4 lakh taxable income, and the Section 87A (available for income up to ₹7 lakh) rebate implies nil liability. Telugu: By taking the old system, all deductions under 80C, HRA and more will make tax zero as well.

Q3. What is the difference between 4.5 LPA and 4.5 LPA CTC?

Both are the same ₹4,50,000 per annum CTC. But CTC has components such as employer PF, gratuity, and other non-cash benefits that you do not get directly. CTC is always > in-hand salary.

Q4. Does clicking on professional tax lower my salary in hand?

Yes, professional tax (PT) is a minor, state-level deduction of ₹150–₹200/month for your salary range. It is automatically deducted from your gross salary and somewhat reduces your take-home. The annual maximum is ₹2,500.

Q5. Q- Will I be given a PF Account at 4.5 LPA?

Yes. All companies with more than 20 employees must register for EPF, regardless of salary. You, along with your employer, deposit 12% of the basic salary (both you and your employer usually ₹1,800/month each) in your EPF account. Paycheck is lower now, but it creates a retirement corpus.

Q6. Best way to calculate my in-hand salary of 4.5 LPA?

So, the formula is In-hand = Gross Monthly Salary − Employee PF − Professional Tax − TDS (if applicable). Get an elaborate salary break-up from your HR before joining in order to get the most realistic figure.

Q7. Is it possible that my in-hand salary for a 4.5 LPA will be different from a colleague’s at the same CTC?

Yes. If your peer is paid on a different salary structure, like a higher basic leading to greater PF deduction and/or more NPS contributions, then even at the same CTC, his in-hand would vary from yours.

Q8. Will 4.5 LPA be enough to afford a home loan?

Most banks allow home loan EMIs equal to 40–50% of net monthly income. On a ₹35,000/month take-home salary, this is capable of supporting an EMI of ₹14,000–17,500/month for a loan size of something like ₹15–18 lakh (20-YR @ 8.5%). This may restrict purchases of metro property, but it will work for houses in smaller cities.

Final Thoughts About 4.5 LPA In Hand Salary

A 4.5 LPA In Hand Salary is usually more exciting than the recognition list, so it’s essential to go by here and know your CTC numbers. In normal scenarios, considering the standard deductions, funds have banked around ₹33k–₹36k/month. This exact number varies per individual according to their employer’s salary structure, the state one is working in (for professional tax), as well as the mode of investment for tax savings.

Always ask for the CTC break-up in detail before taking any offer, and each year, use the old vs new tax regime comparison to find out if you may be losing some money. Earning a zero income tax at 4.5 LPA is possible, making the right structuring of your salary even more important.

Read Also: 9 LPA In-Hand Salary in India

Yashika is the dedicated content writer and salary research author at TheMonthlySalary.com. She specializes in creating clear, helpful, and easy-to-understand content about monthly salary, in-hand pay, salary calculators, career growth, and salary updates. Her goal is to simplify salary-related topics for employees, job seekers, students, and working professionals. Through well-researched guides and practical insights, Yashika helps readers make smarter career and financial decisions.