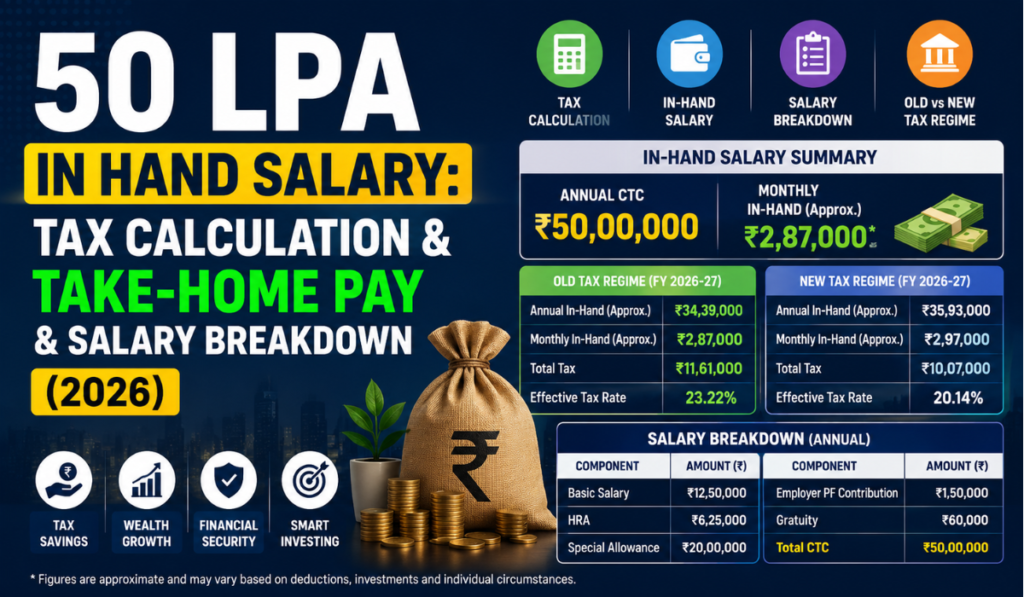

So you earn 50 LPA in hand salary, and that puts you among the top few earners in India, but there is a huge difference between your CTC and what reaches your bank account at the end of every month, usually a difference of ₹10-15 lakhs/ annum. Whether you are reviewing an offer in hand, aligning your finances or just trying to interpret what ’50 LPA in hand salary’ includes, this guide details how the salary structure works and strategies for tax optimisation and long-term wealth creation.

What Does 50 LPA In Hand Salary Actually Mean?

A must-have knowledge of nomenclature to be aware of the Lakhs per Annum (LPA), which means ₹50,00,000 will be your overall payment in a year. But there is a lot of confusion between CTC and in-hand salary, as these are two very different numbers.

CTC (Cost to Company) is the total amount of money an employer spends on you, be it base salary, allowances, PF contribution made by your employer towards EPF, gratuity, insurance premiums, bonus and its tax implication or ESOP (Employee Stock Option Plan).

In-hand salary (take-home) is the amount credited to your bank account after deductions such as income tax (TDS), employee PF contribution, professional tax and a few more deductions.

When someone says ‘₹50 LPA in hand salary ‘, they are usually referring to their actual annual take-home, which is, in reality, ₹50 lakhs p.a and that would mean a CTC much higher, often 65- 75 LPA, depending on the salary structure, bonus components and tax regime chosen.

CTC vs In-Hand: A Sample Breakdown

If your target is ₹50 LPA In Hand Salary then this is what a CTC might look like.

| Component | Annual Amount (₹) | Notes |

| Basic Salary | 24,00,000 | Typically 40-50% of CTC |

| HRA (House Rent Allowance) | 12,00,000 | Usually 40-50% of basic |

| Special Allowance | 18,00,000 | Balancing component |

| Employer PF Contribution | 2,88,000 | 12% of basic, capped or uncapped |

| Gratuity | 1,15,000 | Statutory provision |

| Performance Bonus | 8,00,000 | Variable, often paid annually |

| Total CTC | 66,03,000 | Approximate |

| Less: Employee PF | (2,88,000) | Deducted from salary |

| Less: Income Tax (TDS) | (12,50,000) | Approximate, varies by regime |

| Less: Professional Tax | (2,500) | State-dependent, nominal |

| Approximate In-Hand (Annual) | 50,62,500 | |

| Approximate In-Hand (Monthly) | 4,21,875 |

Read Also: 5.5 LPA In Hand Salary: Monthly Take-Home Pay Calculation 2026

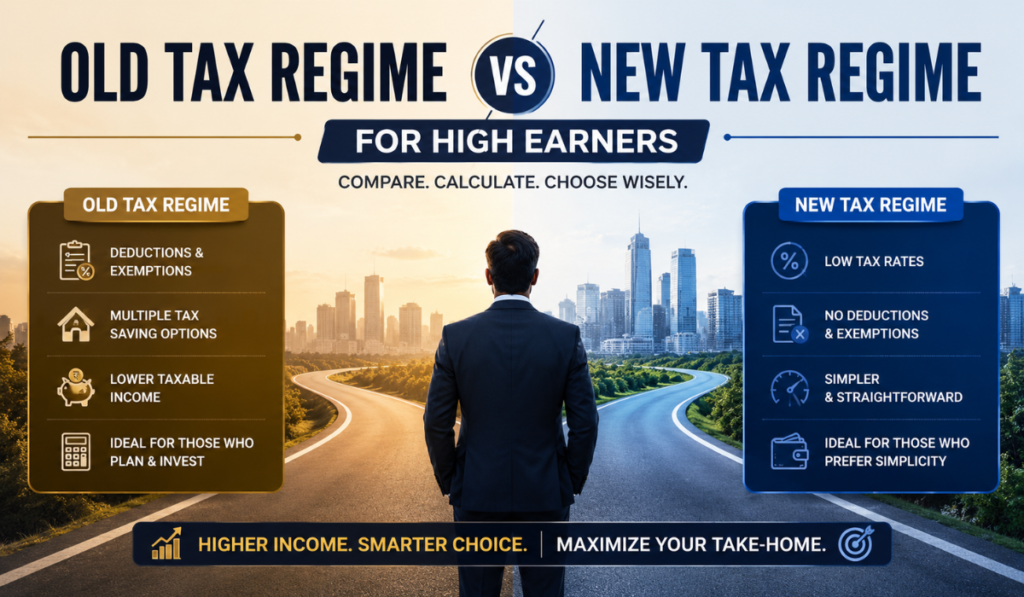

Old Tax Regime vs New Tax Regime for High Earners

This choice between the old or the new tax regime weighs heavily on an individual earning at this level in determining the final in-hand valuation. Here’s a simplified comparison.

| Aspect | Old Tax Regime | New Tax Regime |

| Tax Slabs | Higher slabs but more deductions allowed | Lower slabs, fewer deductions |

| HRA Exemption | Available | Not available |

| Section 80C (₹1.5L) | Available (PPF, ELSS, EPF, life insurance) | Not available |

| Section 80D (Health Insurance) | Available | Not available |

| Standard Deduction | ₹50,000 | ₹75,000 (as per recent revisions) |

| NPS 80CCD(1B) | Available | Not available |

| Home Loan Interest (Section 24) | Available (up to ₹2L) | Not available |

| Best Suited For | Those with significant deductions (home loan, investments, HRA) | Those with minimal deductions or renting without HRA claims |

If you are around the ₹50 LPA in hand salary level and have a home loan, are claiming HRA and also maxing 80C & 80D, the old regime will deliver lower tax outgo due to how much higher the slab rates are in the old vs new for you. On the other hand, the new regime has a lower slab, but if your deductions are few, then the above deduction limit may not add up very well to that. Before making a decision, a CA/tax calculator comparison based on your figures is a must.

Income Tax Calculation at This Level (Old Regime Example)

Here’s How Income Tax is calculated at This Level (example for the old regime):

| Income Slab | Tax Rate | Tax Amount (Approx) |

| Up to ₹2.5 lakh | Nil | 0 |

| ₹2.5L – ₹5L | 5% | 12,500 |

| ₹5L – ₹10L | 20% | 1,00,000 |

| Above ₹10L | 30% | Remaining income × 30% |

| Surcharge | 10-15% | Applicable above ₹50L taxable income |

| Health & Education Cess | 4% | On total tax + surcharge |

You will also be in the surcharge bracket at this income level. An additional 10% will be levied on any taxable income above ₹50 lakh, and 15% if the taxable income is over ₹1 crore. This is a most crucial point: just under or over the ₹50 lakh threshold makes a difference on 2 very important counts (#1 being surcharge), so tax planning (using legitimate ways to optimise taxable income marginally below these thresholds) has value.

Maximising Take-Home: Salary Structuring Tips

These components can help you increase your in-hand value if you are negotiating an offer or looking to restructure your current package:

- House Rent Allowance (HRA)

For those renting, have HRA appropriately sized (generally 40–50% of basics) to maximise exemption on tax when under old regime.

- Leave Travel Allowance (LTA)

LTA is a tax-free exemption for genuine travel-related claims (twice during a block of four years), which helps reduce taxable income.

- Meal Vouchers / Food Allowance

Some organisations provide meal coupons that are tax-free (₹26,400/year through Sodexo-type vouchers), which is a low but legitimate tax-free benefit.

- The post Salary Deduction for National Pension System (NPS) via Employer appeared first on FinTaurant.

Deduction for employer payment made to NPS under 80CCD(2) is exempt up to 10% of basic salary (14% in the case of government employees) and does not count against the ₹1.5 lakh limit under 80C. This is one of the most effective tools available for taxpayers in the highest tax slabs.

- Car Lease / Fuel Reimbursements

If your organisation has a car lease policy, the lease rentals and maintenance are exempt from tax (there will be some taxable value depending upon the category of car), thus bringing down taxable salary.

- Telephone and Internet Reimbursements

Telecom and internet bill reimbursements (with supporting documents) are tax-free, generally overlooked fringe benefits.

Read Also: 7.5 LPA In Hand Salary: Breakdown, Deductions, Tax Impact

Tax-Saving Investment Options for 50 LPA In Hand Salary Earners (Old Regime)

| Instrument | Section | Maximum Limit | Lock-in / Notes |

| EPF (mandatory) | 80C | Part of ₹1.5L combined limit | Until retirement |

| PPF | 80C | ₹1.5L combined | 15 years |

| ELSS Mutual Funds | 80C | ₹1.5L combined | 3 years |

| Life Insurance Premium | 80C | ₹1.5L combined | Policy term |

| NPS (self-contribution) | 80CCD(1B) | Additional ₹50,000 | Until retirement |

| NPS (employer contribution) | 80CCD(2) | Up to 10% of basic | Until retirement |

| Health Insurance Premium | 80D | ₹25,000 (self) + ₹50,000 (parents senior citizens) | Annual |

| Home Loan Interest | 24(b) | ₹2,00,000 | Property-dependent |

| Home Loan Principal | 80C | Part of ₹1.5L combined | Property-dependent |

At this level of income, deductions on 80C (₹1.5L), if any under 80CCD(1B) (₹50,000), 80D (₹25,000-₹75,000 depending on parents’ age), and home loan interest ₹2L (if any), can together save them ₹4–4.5 lakhs in taxable income leading to an annual tax saving of ~₹1.2–1.4 lakhs at the 30% slab + surcharge!

Wealth-Building Strategy for ₹50 LPA In Hand Salary Earners

If expenses are managed well, there is tremendous wealth creation potential with a monthly in-hand of around ₹4.2 lakhs. Below is a template for the distribution of allocations over the month:

| Category | Percentage | Monthly Amount (₹) | Details |

| Essential Expenses | 25-30% | 1,05,000 – 1,26,000 | Rent/EMI, utilities, groceries |

| Lifestyle & Discretionary | 15-20% | 63,000 – 84,000 | Dining, travel, entertainment |

| Investments (Equity) | 25-30% | 1,05,000 – 1,26,000 | Mutual funds, stocks, direct equity |

| Debt Instruments (PPF, NPS, Bonds) | 10% | 42,000 | Tax-efficient safe investments |

| Emergency Fund / Liquid | 5% | 21,000 | Until 6-12 months, expenses are covered |

| Insurance (Term + Health) | 2-3% | 8,000 – 12,000 | Adequate coverage |

Recommended Investment Mix for Long-Term Growth

| Asset Class | Allocation | Rationale |

| Equity Mutual Funds (Index + Active) | 50-60% | Long-term growth, tax-efficient (LTCG) |

| Direct Equity / Stocks | 10-15% | Higher growth potential for experienced investors |

| Debt Funds / Bonds | 10-15% | Stability and diversification |

| Real Estate (if applicable) | Variable | Often a major asset but illiquid |

| Gold / SGBs | 5% | Inflation hedge |

| International Equity (US markets via funds) | 5-10% | Currency diversification, global exposure |

Even if you invest ₹1-1.2 lakh every month into equity-oriented instruments at 11-12% annually which would amount to be in excess of ₹3–4 crores over the next 15 years and far far more over a haunt of 20-25 years which should not be beyond someone in early-to-mid career still earning up to this level (at ₹50 LPA in hand salary) can achieve.

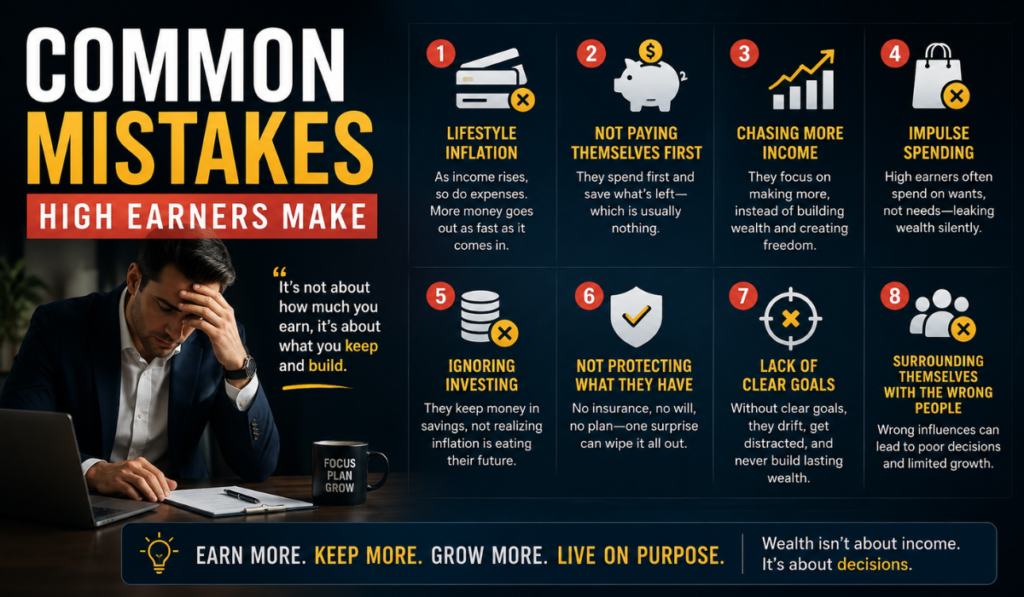

Common Mistakes High Earners Make

Lifestyle inflation is outpacing income growth. As your income goes up, your expenses also increase, often in a dollar-for-dollar or faster-than-growth pattern, which creates an expense burden on the excess surplus to invest.

- While the surcharge limits threshold is ₹50L or ₹1 crore taxable income, when crossed means you move into bigger surcharge zones, so some planning to be efficient around these makes sense.

- Dependence on EPF/PPF only, though safe, will not be sufficient in beating inflation enough for wealth creation at this income level; exposure to equities is critical!

- No or low insurance despite high salary, a life cover of at least 15-20x annual in-hand income + sizeable health policy (₹50L-₹1Cr cover) is basic, irrespective of how much you earn

- Ignoring salary structure: Most employees don’t even optimise their CTC breakup for tax efficiency and can save lakhs in a legit way each year with a structured CTC.

Read Also: Income Tax Officer Salary 2026

Frequently Asked Questions (FAQ): 50 LPA In Hand Salary

Q1: CTC required to get ₹50 LPA in hand salary?

Based on the tax regime and salary structure, a CTC of around ₹65-75 LPA is generally required to deliver roughly ₹50 LPA in hand salary annually (take-home) amount, after accounting for income tax, PF contributions and other statutory deductions.

Q2: Is ₹50 LPA in hand salary good in India?

Yes, you are now correct in assuming that this puts one quite sumptuously within the top bracket of earners in India or about ₹4 lakh every month after tax and more than double the national average income and even eclipsing most metro city salary benchmarks for senior professional industry roles.

Q3: What is the taxation on ₹50 LPA in hand salary?

Assuming an in-hand (post-tax) figure of ₹₹50 LPA in hand salary, your gross taxable would probably be somewhere between ₹62-70 lakh and total tax (including surcharge and cess), depending on the regime and deductions claimed, is usually around 12-16 lakhs annually.

Q4: Should I opt for an old or new tax regime at this income level?

While the slab rates might seem to be higher under the new regime, if you have large deductions such as home loan interest, HRA claims, etc., till 31st March, then in most cases, the old regime should work better. However, if you have little in the way of deductions, then the lower rates offered under the new regime may put you on par or even better off. One of the best ways to do this is by inputting your real details into an income tax calculator and comparing the figures year on year

Q5: What is the best way to save tax when my ₹50 LPA in hand salary?

Important aspects now are full utilisation of 80C (₹1.5L), NPS under 80CCD(1B) and 80CCD(2), HRA if renting, home loan interest if applicable, health insurance-80D to be optimised, salary composition with LTA, meal vouchers, telephone reimbursements, etc should also be done suitably.

Q6: What amount to invest every month is good for that income level?

As a general thumb rule, typically 25-30% of monthly in-hand salary is invested, which at ₹4.2 lakh in-hand, works out to around ₹1-1.25 lakh/month going into equity mutual funds, NPS, PPF and other long-term instruments.

Q7: ₹50 lakh surcharge limit apply to in-hand salary or CTC?

The surcharge slab is applicable to your taxable income (after deduction) and not directly on your CTC or in-hand salary. In this case, you pay 10% outside on the tax if your taxable income is over ₹50 lakh, and then an increase of 15% above ₹1 crore.

Q8: I have ₹50 LPA In Hand Salary, so how much insurance do I need?

Ultimately, a good rule of thumb is 15-20x your take-home salary in term plan cover (₹7.5-10 crores in this case) and ₹50 lakh to 1 crore minimum health cover especially for floater plans, given the ballooning healthcare costs these days.

Final Thoughts About 50 LPA In Hand Salary

An in-hand pay of ₹50 LPA In Hand Salary is significant earning potential, but the real financial benefit depends partly on how the CTC is framed, what tax regime and how disciplined you invest. The triad of knowing the difference between CTC and in-hand salary, optimal structuring of salary heads for tax efficiency and directing a significant percentage of take-home pay into life-long wealth generation through long-term equity-based investments is how to convert high income into permanent wealth. You need to plan well; however, if you earn around this level today, building a portfolio worth crores is a very doable goal within 15-20 years with an acceptable lifestyle in the current environment.

Yashika is the dedicated content writer and salary research author at TheMonthlySalary.com. She specializes in creating clear, helpful, and easy-to-understand content about monthly salary, in-hand pay, salary calculators, career growth, and salary updates. Her goal is to simplify salary-related topics for employees, job seekers, students, and working professionals. Through well-researched guides and practical insights, Yashika helps readers make smarter career and financial decisions.