The most frequently asked question by every job seeker and fresher in India is What does the 7.5 LPA In Hand Salary mean? What may seem like a high CTC on paper can vary drastically in terms of what actually gets deposited in your bank account monthly. Having a clear idea of how your in-hand salary, after provident fund, income tax, professional tax and various other components, comes out to be 7.5 LPA is imperative for financial planning.

This ultimate guide takes you through all the steps in a 7.5 LPA in hand salary computation, including gross salary breakdown, monthly take-home, government tax slabs and some real-life tips on how to increase your net earnings. This article would be a complete no-nonsense clarity, whether you are a fresher who just got an opportunity, or you are a mid-level professional benchmarking your compensation.

What Does 7.5 LPA Mean?

This is the full form of LPA, which means Lakhs Per Annum, i.e., this is how your overall salary package would be structured in INR on an annual basis. CTC for a 7.5 LPA Salary is ₹7,50,000 per annum. But CTC is not your take-home or in-hand salary. CTC consists of several items that are either charged before dispersing the salary or disbursed as in-kind benefits.

7.5 LPA in hand salary means the take-home you get every month in your bank after all the statutory and voluntary deductions are made from your gross salary.

CTC vs. Gross Salary vs. In-Hand Salary – Key Differences

| Term | Definition | Example (7.5 LPA) |

| CTC (Cost to Company) | Total annual cost borne by the employer, including all benefits and contributions | ₹7,50,000 per year |

| Gross Salary | CTC minus the employer’s PF contribution and other non-salary benefits | ₹6,84,000 – ₹7,10,000 per year |

| Net / In-Hand Salary | Gross salary minus all employee deductions (PF, tax, PT) | ₹48,000 – ₹55,000 per month |

| Monthly CTC | CTC divided by 12 months | ₹62,500 per month |

| Monthly Gross | Gross annual salary divided by 12 | ₹57,000 – ₹59,200 per month |

The difference between the monthly CTC figure (₹62,500) and the actual 7.5 LPA take-home pay is due to the employer Provident Fund contribution (offered under CTC but not paid into your hand), employee PF deduction, income tax (TDS), as well as professional tax.

Read Also: Income Tax Officer Salary 2026

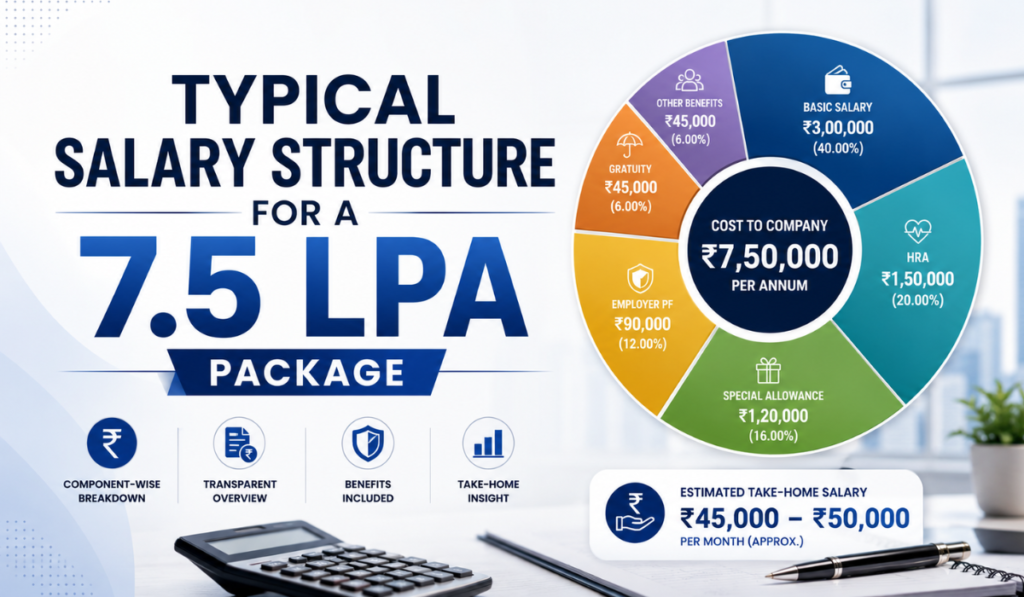

Typical Salary Structure for a 7.5 LPA Package

In fact, most of the Indian companies divide CTC into different components. To calculate your 7.5 LPA in hand salary step by step, you need to understand each component explained below. Here is a standard salary structure breakup that most IT companies, startups and corporates follow in India:

Monthly Salary Component Breakdown (7.5 LPA CTC)

| Salary Component | Monthly Amount (INR) | Annual Amount (INR) | % of CTC |

| Basic Salary (40–50% of CTC) | ₹25,000 – ₹31,250 | ₹3,00,000 – ₹3,75,000 | 40–50% |

| House Rent Allowance (HRA – 40–50% of Basic) | ₹10,000 – ₹15,625 | ₹1,20,000 – ₹1,87,500 | 16–25% |

| Special Allowance | ₹10,000 – ₹15,000 | ₹1,20,000 – ₹1,80,000 | 16–24% |

| Leave Travel Allowance (LTA) | ₹1,500 – ₹2,500 | ₹18,000 – ₹30,000 | 2–4% |

| Medical Allowance | ₹1,250 | ₹15,000 | 2% |

| Employer PF Contribution (12% of Basic) | ₹3,000 – ₹3,750 | ₹36,000 – ₹45,000 | 4.8–6% |

| Gratuity (4.81% of Basic) | ₹1,200 – ₹1,503 | ₹14,430 – ₹18,038 | 1.9–2.4% |

| Performance Bonus (if annual) | ₹3,000 – ₹6,250 | ₹36,000 – ₹75,000 | 4.8–10% |

| TOTAL CTC | ₹62,500 | ₹7,50,000 | 100% |

Please note: the breakdown differs slightly from employer to employer. Higher Basic Salary will also lead to Higher PF deductions, but it will also help you in building a bigger PF Corpus. Startups generally give a high Special Allowance and a low Basic to minimise PF liability, which in turn increases the net salary.

Deductions That Reduce Your 7.5 LPA In Hand Salary

Before the net amount lands in your bank account, the following deductions are made from that gross monthly salary. These are the main parameters which will give you the true 7.5 LPA in hand salary

Monthly Deductions Breakdown

| Deduction | Basis | Monthly Amount (INR) | Annual Amount (INR) |

| Employee PF (EPF) | 12% of Basic Salary | ₹1,800 – ₹3,750 | ₹21,600 – ₹45,000 |

| Income Tax (TDS) | Based on the tax slab | ₹1,500 – ₹4,500 | ₹18,000 – ₹54,000 |

| Professional Tax | State-specific (up to ₹200/month) | ₹0 – ₹200 | ₹0 – ₹2,400 |

| Employee State Insurance (ESIC) | Only if gross < ₹21,000/month, N/A here | ₹0 | ₹0 |

| Health Insurance Premium | If deducted at source | ₹0 – ₹1,500 | ₹0 – ₹18,000 |

| NPS Contribution (optional) | Voluntary | ₹0 – ₹2,000 | ₹0 – ₹24,000 |

| TOTAL DEDUCTIONS (approx.) | – | ₹4,500 – ₹10,000 | ₹54,000 – ₹1,20,000 |

A 7.5 LPA In Hand Salary package would not come under ESIC because the gross monthly salary will be more than ₹21,000, and ₹21,000 is currently the ESIC cap line for eligibility. Employee PF contribution is 12% of Basic Salary (capped at ₹1,800/month if Basic > ₹15,000, but most companies apply full 12% without cap).

7.5 LPA In Hand Salary – Actual Monthly Take-Home Calculation

Now, let us compute the actual 7.5 LPA In Hand Salary under two typical situations; one is a company keeps Basic Salary to be 40% of the CTC, and in the other it keep at 50% of the CTC.

Scenario A – Basic Salary at 40% of CTC (₹25,000/month)

| Item | Monthly (INR) | Annual (INR) |

| Gross Monthly Salary (CTC minus Employer PF & Gratuity) | ₹57,200 | ₹6,86,400 |

| Less: Employee PF (12% of ₹25,000) | – ₹3,000 | – ₹36,000 |

| Less: Income Tax (TDS – New Regime) | – ₹1,667 | – ₹20,000 |

| Less: Professional Tax | – ₹200 | – ₹2,400 |

| NET IN-HAND SALARY (Scenario A) | ₹52,333 | ₹6,28,000 |

Scenario B – Basic Salary at 50% of CTC (₹31,250/month)

| Item | Monthly (INR) | Annual (INR) |

| Gross Monthly Salary (CTC minus Employer PF & Gratuity) | ₹55,000 | ₹6,60,000 |

| Less: Employee PF (12% of ₹31,250, capped at ₹1,800) | – ₹1,800 | – ₹21,600 |

| Less: Income Tax (TDS – New Regime) | – ₹1,667 | – ₹20,000 |

| Less: Professional Tax | – ₹200 | – ₹2,400 |

| NET IN-HAND SALARY (Scenario B) | ₹51,333 | ₹6,16,000 |

The 7.5 LPA in hand salary usually ranges around ₹50,000 – ₹54,000 monthly under the new tax regime after standard deductions (as these scenarios suggest). The number would differ based on your Basic Salary per cent, tax regime opted for and any other deductions made by your employer.

Read Also: Anjana Om Kashyap Salary 2026: Income, Career & Net Worth

Income Tax Calculation on 7.5 LPA – Old vs. New Regime

India follows two regimes of income tax: the Old Tax Regime and the New Tax Regime (applicable for FY 2024-25 onwards). The regime you choose has a huge impact on your 7.5 LPA in-hand salary.

New Tax Regime – Tax Slabs (FY 2025-26)

| Annual Income Slab | Tax Rate |

| Up to ₹3,00,000 | Nil |

| ₹3,00,001 – ₹7,00,000 | 5% |

| ₹7,00,001 – ₹10,00,000 | 10% |

| ₹10,00,001 – ₹12,00,000 | 15% |

| ₹12,00,001 – ₹15,00,000 | 20% |

| Above ₹15,00,000 | 30% |

Tax Calculation on 7.5 LPA – Old Regime vs. New Regime

| Particulars | Old Tax Regime (INR) | New Tax Regime (INR) |

| Gross Taxable Income | ₹7,50,000 | ₹7,50,000 |

| Standard Deduction | – ₹50,000 | – ₹75,000 (FY25-26) |

| 80C Deductions (PF + ELSS + PPF etc.) | – ₹1,50,000 | Not applicable |

| 80D (Health Insurance Premium) | – ₹25,000 | Not applicable |

| HRA Exemption (metro city, 40% of Basic) | – ₹1,00,000 (approx) | Not applicable |

| Net Taxable Income | ₹4,25,000 | ₹6,75,000 |

| Income Tax | ₹8,750 | ₹18,750 |

| Health & Education Cess (4%) | ₹350 | ₹750 |

| TOTAL TAX PAYABLE | ₹9,100 | ₹19,500 |

| Monthly TDS | ₹758 | ₹1,625 |

The Old Tax Regime offers a highly lower tax liability on a salary of 7.5 LPA if you make full use of Section 80C, 80D, and the HRA exemptions. But, if you do not have such investments or deductions regulated in place, the New Tax Regime emerge as easier and possibly almost equal in overall tax outgo. Starting from FY 2024-25, the New Tax Regime is the default; you need to opt for the Old Regime explicitly while filing your ITR.

Is 7.5 LPA In Hand Salary Good in India? City-Wise Perspective

Wherever you tend to reside to work, your 7.5 LPA in hand salary is worth something different when it comes to purchasing power. This is how a monthly take-home of around ₹51,000 – ₹54,000 stacks up against the average cost of living in India when we break down all these costs city-wise:

| City | Avg. Rent (1BHK) | Monthly Living Cost (Single) | Monthly Savings Potential | Comfort Level |

| Mumbai | ₹20,000 – ₹35,000 | ₹45,000 – ₹55,000 | ₹0 – ₹8,000 | Tight |

| Bangalore | ₹15,000 – ₹25,000 | ₹35,000 – ₹45,000 | ₹8,000 – ₹18,000 | Comfortable |

| Delhi NCR | ₹12,000 – ₹22,000 | ₹30,000 – ₹42,000 | ₹10,000 – ₹22,000 | Good |

| Pune | ₹10,000 – ₹18,000 | ₹28,000 – ₹38,000 | ₹14,000 – ₹24,000 | Very Good |

| Hyderabad | ₹10,000 – ₹16,000 | ₹26,000 – ₹36,000 | ₹16,000 – ₹26,000 | Excellent |

| Chennai | ₹10,000 – ₹18,000 | ₹28,000 – ₹38,000 | ₹14,000 – ₹24,000 | Very Good |

| Kolkata | ₹7,000 – ₹14,000 | ₹22,000 – ₹32,000 | ₹20,000 – ₹30,000 | Excellent |

| Tier-2 Cities | ₹5,000 – ₹10,000 | ₹18,000 – ₹26,000 | ₹25,000 – ₹34,000 | Outstanding |

Most cities of India (excluding Mumbai) would consider a 7.5 LPA in hand salary a decent amount to sustain yourself with. However, in metro cities like Bangalore, Delhi NCR, Pune and Hyderabad, it enables you to lead a comfortable life with substantial savings opportunities. Mumbai has a high cost of living (such as rent), so it is quite tight but achievable if sharing.

Read Also: 3.6 LPA In Hand Salary: Breakdown, Deductions, Tax Impact

How to Increase Your 7.5 LPA In Hand Salary

Though the gross CTC is constant, there are various legal and strategic methods to increase your take-home pay each month for a package of 7.5 LPA.

- Choose the Old Tax Regime and make bare minimum Section 80C investments (Equity Linked Savings Schemes (ELSS), Public Provident Fund (PPF), Employees’ Provident Fund and Miscellaneous Provisions Act, 1952(EPF), National Savings Certificate(NSC), two additional tax-saving fixed deposits(FDs) up to ₹1,50,000 per annum. For a 7.5 LPA earner alone, this can save ₹15,000 – ₹30,000 of annual tax.

- If you are living in a rented house, claim an HRA exemption. Offer your employer rent receipts to slash the taxable income considerably.

- Travel Expenses: Use Leave Travel Allowance (LTA) for actual expenses or travel, as it is fully exempt under Section 10(5), and there are two journeys allowed every block of four calendar years.

- Higher Special Allowance and a lower Basic Salary structure (if your employer allows the restructuring). It implies lesser PF deduction with a larger amount in hand every month.

- NPS (National Pension System) under Section 80CCD(1B) Here you can invest in NPS to get an extra ₹50,000 deduction above the limit of 80C.

- Tax-free food allowance/meal vouchers office (Sodexo or similar): ₹50/meal for 2 meals x 22 working days x 12 months = ₹26,400 per year

- Prescribe Form 12B while joining the new employer in mid-financial year for safeguarding against unnecessary TDS deductions by the second employer.

- Home Loan for House Property Note – Claim deduction under Section 24 (b) of ₹2,00,000 per Annum in case a loan is secured. Old Regime

Salary Growth Projection from 7.5 LPA

A package of 7.5 LPA in hand salary is mostly found in the 1–4 years of experience range in IT, banking, analytics & consulting sectors. Hyper-realistic hypothetical Salary jump in case of 10–20% annual salary hikes.

| Year | Expected CTC (LPA) | In-Hand Monthly (INR) | Experience Bracket |

| Current | ₹7.5 LPA | ₹51,000 – ₹54,000 | 1–3 years |

| Year 1 (10% hike) | ₹8.25 LPA | ₹56,000 – ₹60,000 | 2–4 years |

| Year 2 (15% hike) | ₹9.5 LPA | ₹64,000 – ₹69,000 | 3–5 years |

| Year 3 (20% hike) | ₹11.4 LPA | ₹76,000 – ₹82,000 | 4–6 years |

| Year 5 (consistent 15%) | ₹15 LPA | ₹98,000 – ₹1,05,000 | 6–8 years |

| Year 7 (consistent 15%) | ₹20 LPA+ | ₹1,30,000 – ₹1,40,000 | 8–10 years |

Companies are engineered to give only 12–15% salary hikes in an annual appraisal cycle, and it is common wisdom that switching companies around every 2–3 years gives a drastic hike of about 25-40%. Even professionals who joined at 7.5 LPA in software development, data science or financial analysis often reach nearly 15–20 LPA through job switches + internal changes within 5 years.

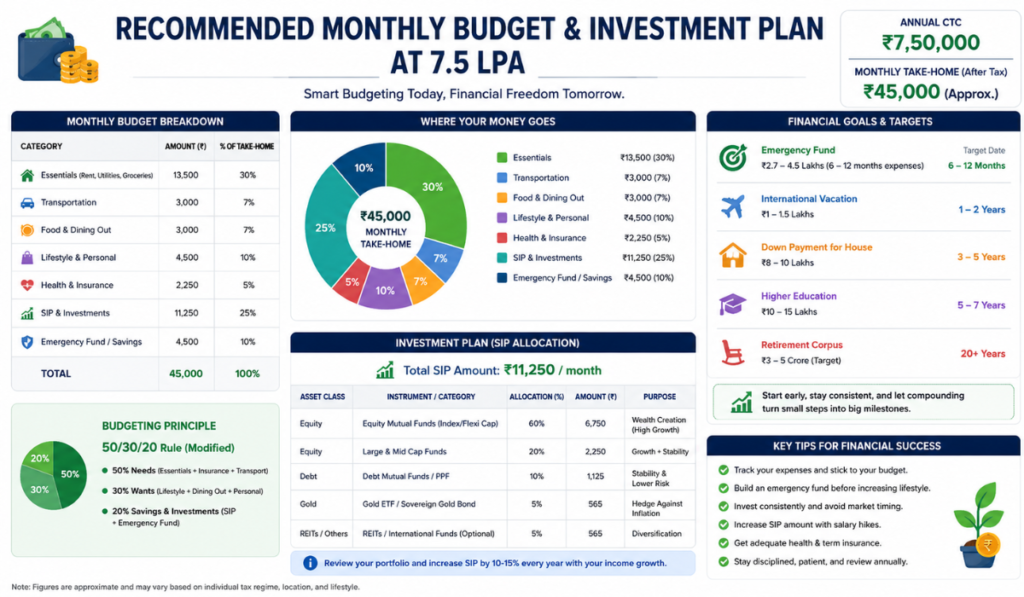

Recommended Monthly Budget & Investment Plan at 7.5 LPA

As a rough conservative monthly salary distribution for anyone getting around 5.2L @7.5LPA in hand and living in a Tier-1 city, it’s comme suivant:

| Category | Monthly Amount (INR) | % of In-Hand | Recommended Approach |

| Rent | ₹12,000 – ₹16,000 | 23–31% | 1BHK or shared in a good locality |

| Groceries & Food | ₹6,000 – ₹9,000 | 12–17% | Cook at home, limit eating out |

| Transport & Commute | ₹2,000 – ₹4,000 | 4–8% | Metro + occasional cab |

| Utilities & Internet | ₹1,500 – ₹2,500 | 3–5% | Broadband + electricity |

| Entertainment & Lifestyle | ₹3,000 – ₹5,000 | 6–10% | OTT, dining out, outings |

| SIP / Mutual Funds | ₹8,000 – ₹12,000 | 15–23% | Index funds + flexi-cap |

| Emergency Fund (liquid) | ₹3,000 – ₹5,000 | 6–10% | Liquid fund or savings account |

| PPF / ELSS (Tax Saving) | ₹4,000 – ₹6,000 | Top-up plan if employer covers the basic | Maximise 80C benefit |

| Health Insurance | ₹1,000 – ₹2,000 | 2–4% | Top-up plan if the employer covers the basic |

| Miscellaneous / Travel | ₹2,000 – ₹4,000 | 4–8% | Annual travel, personal purchases |

Financial planners suggest saving and investing a minimum of 25–30% of your actual take-home salary. A ₹7.5 LPA in hand salary of ₹52,000/month means that it is about going into investments and savings of ₹13,000 – ₹15,600 per month every month, which makes a great start on the long road to financial independence!

Read Also: 30 LPA In Hand Salary: Monthly Salary, Tax

Frequently Asked Questions (FAQs): 7.5 LPA In Hand Salary

Q1. What will the in-hand salary be for 7.5 LPA?

In-hand monthly salary of 7.5 LPA is around ₹50,000 – ₹54,000 under the New Tax Regime or ₹52,000 – ₹56,000 under the Old Tax Regime with full 80C and HRA claims made. It depends mainly on the part of your component, i.e., Basic Salary, the city you are working in (since professional tax may vary from state to state), and what salary structure your employer has coming.

Q2. How much income tax do I have to pay on 7.5 LPA?

For comparison, taxable income for a 7.5 LPA earner is around ₹19,500-22,000 per annum after standard deduction of ₹75000 under the New Tax Regime (FY 2025-26). Using maximum deductions for the Old Tax Regime (80C, 80D, HRA), the total tax can be brought down to ₹8,000 – ₹12,000 annually. The monthly TDS will be ₹700 – ₹1,800 depending on the regime

Q3. In 2025, is 7.5 LPA a good salary in India?

Yes, 7.5 LPA is a good salary in India for jobs which fall under the category of zero to four years experienced jobs by 2025. That puts you in the comfortable range of the top 10–15% of earners with a salary in this country. It provided a great lifestyle with substantial saving potential in tier-2 cities. It is not very expensive, but it does require budgeting in metros like Mumbai.

Q4. How much PF Deduction on 7.5 LPA?

This Deduction can be calculated based on the Basic Salary. For example, if Basic is ₹25,000/month, employee PF = ₹3,000/month (12% of ₹25,000). This is capped at ₹1,800/month if Basic as of the date of applicability of this rule is ₹15,000/- or less. The employer matches that amount, but that is included in CTC and not deducted from your take-home.

Q5. Which one is a better tax regime for 7.5 LPA?

When you earn a 7.5 LPA salary, Old Tax Regime is generally better if you have: ₹1.5 lakh in section 80C investments, ₹25,000 in 80D (health insurance) and HRA exemption for paying rent in the metro city Without these deductions facility, even the New Tax Regime (with a greater standard deduction of ₹75,000 from FY 2024-25), is almost as simple or perhaps better.

Q6. What is my in-hand for 7.5 LPA without PF deduction?

It is worth noting that a few companies especially Start-ups and Small companies do not deduct PF if the Basic Salary remains below ₹15,000/month or employees voluntarily opt out (in case of high basic >₹15K) Here the deduction of ₹1,800 – ₹3,000 PF per month is saved because the 7.5 LPA in hand salary can touch ₹54,000 – ₹57,000 per month.

Q7. How good is 7.5 LPA compared to the average salary in India?

The average salary income in India for the mass-market salaried employee class is ₹2.5 LPA – ₹ 4 LPA. A 7.5 LPA in hand salary is almost double that, or 2–3x the national average and puts you as an earning individual well below median income levels. It is a competitive entry to mid-level compensation among urban white-collar workers.

Q8. How to calculate in-hand salary for a 7.5 LPA government employee?

Salaries of all government employees are given on the basis of the 7th Pay Commission, while private sector CTC is calculated in a different way. The government employee with a gross CTC of around 7.5 LPA may find himself/herself at Pay Level 6 or 7 (Basic Pay ₹35,400 – ₹44,900). In-hand for state employees is also different based upon HRA city classification, DA (now nearly 50%), transport allowance and NPS contribution.

Conclusion For 7.5 LPA In Hand Salary

Calculating what your in-hand salary of 7.5 LPA translates to is more than just dividing ₹7,50,000 by 12. Real monthly take-home. The salary structure, income tax regime chosen, employer PF policy and state you are working in decide the real monthly take home. Here is what you need to be aware of about the salary after tax deduction or in-hand salary derived from a 7.5 LPA: Should work out to ₹50,000 – ₹54,000 per month.

It is a decent paycheck that, assuming prudent budgeting and tax planning in place, allows covering an urban lifestyle with plenty left over to grow generational wealth via disciplined contributions. Select the correct tax regime, maximise exemptions available and structure your salary components correctly to squeeze out an actual difference of ₹55,000 – ₹57,000 from the same 7.5 LPA CTC line item.

Complicated sounds right when it comes to a 7.5 LPA in hand salary, so whether you are assessing a job offer, budgeting your month or just trying your best to understand line-by-line deduction on payslip, this guide shall clarify the entire picture of what an in-hand salary per year of 7.5 lakhs means for your finances in the year 2025.

Yashika is the dedicated content writer and salary research author at TheMonthlySalary.com. She specializes in creating clear, helpful, and easy-to-understand content about monthly salary, in-hand pay, salary calculators, career growth, and salary updates. Her goal is to simplify salary-related topics for employees, job seekers, students, and working professionals. Through well-researched guides and practical insights, Yashika helps readers make smarter career and financial decisions.