When a company gives you a 30 LPA, the number on your offer letter is not what you will actually see in your bank account every month. The 30 LPA in hand salary is your real monthly pay out after applying income tax, Provident Fund contribution and professional tax, as we mentioned earlier, along with gratuity and other statutory obligations.

Knowing the difference between CTC (Cost to Company) and in-hand salary is perhaps one of the biggest financial literacy lessons that any working professional must learn in India. CTC is your employer’s total annual cost of employing you: it is the sum of your salary plus the employer’s PF contributions, gratuity fund provisions, insurance premiums and bonuses. In contrast, your in-hand salary is the amount you receive in your bank account net.

The in-hand monthly CTC salary is normally between ₹1,67,000 to ₹1,90,000 for a 30 LPA CTC, depending on the tax regime, salary structure and deductions claimed. In this guide, we try to explain every rupee ( from your offer letter to your bank) so that you have absolute clarity on how much of the 30 LPA salary in hand, you actually take home.

Understanding CTC vs Gross Salary vs In-Hand Salary

Now, before we get to its calculation, you should understand three terms that are confused with each other:

CTC (Cost to Company): The total annual expense incurred by your employer for hiring you. This encompasses anything from all the contributions and benefits to provisions you may never see in your bank account.

Gross Salary: Gross salary, which is the amount earned before deductions, but after excluding the employer/s share of PF and gratuity from CTC. That’s the gross profit amount that shows up on your payslip before any taxes

In-Hand / Take-Home Salary: The amount that is paid to your bank account after deducting employee PF, professional tax and income tax (TDS) from gross salary; the figure you mostly get.

The formula is simple: In-Hand = Gross Salary, Employee PF, Professional Tax, Income Tax (TDS). In packages of ₹20–40 LPA, the CTC and in-hand salary difference usually lies between 25–35%.

Salary Structure Breakdown for 30 LPA CTC

The typical salary structure in the table below is a 30 LPA In Hand Salary package whose Basic Salary accounts for 40% of CTC (common corporate structure):

| Salary Component | Annual Amount (₹) | Monthly Amount (₹) | % of CTC |

| Basic Salary (40%) | 12,00,000 | 1,00,000 | 40% |

| House Rent Allowance (40% of Basic) | 4,80,000 | 40,000 | 16% |

| Special Allowance | 8,52,552 | 71,046 | 28.4% |

| Employer PF Contribution (12% of Basic) | 1,44,000 | 12,000 | 4.8% |

| Gratuity (4.81% of Basic) | 57,720 | 4,810 | 1.9% |

| Performance Bonus | 2,40,000 | 20,000 | 8% |

| Medical / Health Insurance | 25,728 | 2,144 | 0.9% |

| TOTAL CTC | 30,00,000 | 2,50,000 | 100% |

Note: Employer PF and Gratuity are part of CTC but are NOT credited to your bank account monthly. Employer PF goes into your EPF account; gratuity is paid as a lump sum only after 5 years of service.

Read Also: 14 LPA In Hand Salary

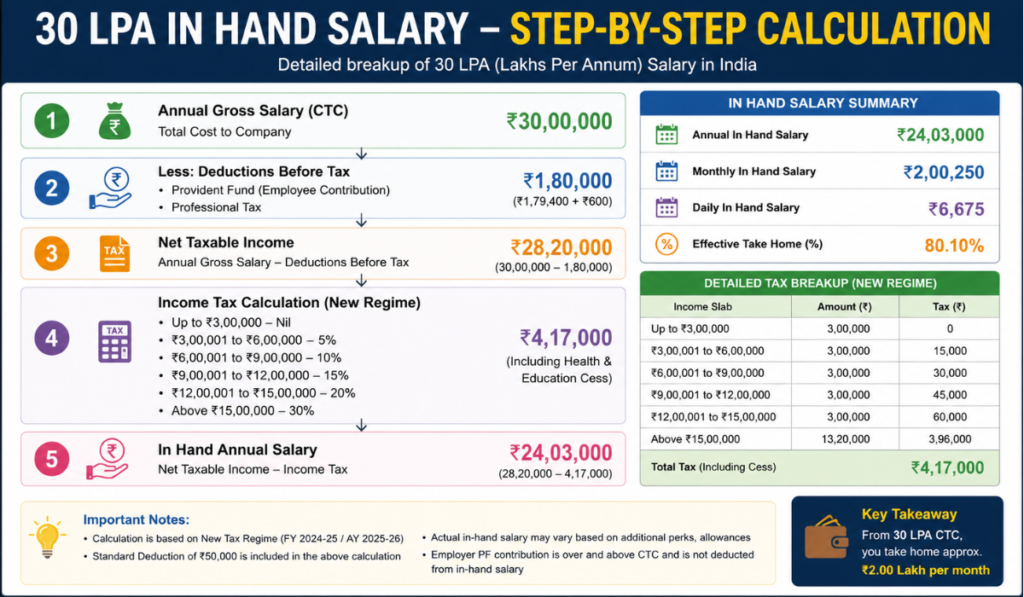

Step-by-Step Calculation: 30 LPA In Hand Salary

Step 1 – Identify Gross Monthly Salary

Deduct Employer PF (₹1,44,000) and Gratuity (₹57,720) from the ₹30,00,000 CTC. This results in a gross annual salary of about ₹27,98,280 or ₹2,33,190 per month. This shows up as gross on your payslip.

Step 2 – Apply Employee-Side Deductions

And then these statutory deductions from your gross monthly salary: Employee PF (₹12,000/month at ₹1,00,000), Professional Tax ₹200/month standard for most states and TDS.

Step 3 – Compute Income Tax

In the New Tax Regime FY 2026-27, you have a standard deduction of ₹75,000, so your income after the standard deduction is ₹29,25,000. Then the tax is calculated based on the slab rates, which are in a progressive manner. Tax before cess is ₹4,57,500. Including Health & Education Cess at 4% (₹18,300), the total annual tax liability is ₹4,75,800 and TDS monthly deduction comes out to around ₹39,650.

All Deductions at a Glance (30 LPA)

| Deduction Head | Annual (₹) | Monthly (₹) | Remarks |

| Employee PF (12% of Basic) | 1,44,000 | 12,000 | Goes to EPF account |

| Employer PF (12% of Basic) | 1,44,000 | 12,000 | Part of CTC, not take-home |

| Gratuity | 57,720 | 4,810 | Paid after 5 yrs service |

| Professional Tax | 2,400 | 200 | Most states ₹200/month |

| Income Tax (New Regime) | 4,75,800 | 39,650 | After ₹75,000 std deduction |

| Health & Education Cess (4%) | 18,300 | 1,525 | On income tax |

| Group Health Insurance Premium | 25,728 | 2,144 | Varies by employer |

| TOTAL DEDUCTIONS | 8,67,948 | 72,329 | Approx. 28.9% of CTC |

New Tax Regime vs Old Tax Regime: Which is Better at 30 LPA?

One of the most common decisions for a 30 LPA In Hand Salary earner is whether he or she should switch to the New Tax Regime (this will remain the default regime from FY 2025-26) or not. It replaces lower slab rates with virtually no exemptions under the new regime. The previous system permits deductions such as those for 80C, HRA and home loan interest, but levies taxes on income at higher rates.

For the New Tax Regime, the slab rates for FY 2026-27 are as follows: 0% on up to ₹4 lakh; 5% on ₹4–8 lakh; 10% on ₹8–12 lakh; 15% on ₹12–16 lakh; 20% on ₹16–20 lakh; 25% between ₹20 and ₹24 Lakh, while those reading more than that will have to pay a tax of30%.

The old regime may provide higher deductions for a 30 LPA earner who fully utilises 80C investments (PPF, ELSS, LIC, home loan principal), HRA in a metro city and health insurance covered under 80D. Nonetheless, after accounting for all these exemptions, the New Tax Regime saves most salaried professionals in this bracket about ₹1,71,600 per year.

New Tax Regime vs Old Tax Regime Comparison (30 LPA)

| Particulars | New Tax Regime (FY 2026-27) | Old Tax Regime (FY 2026-27) |

| Gross Taxable Income | ₹30,00,000 | ₹30,00,000 |

| Standard Deduction | ₹75,000 | ₹50,000 |

| Section 80C Deduction | Not Available | Up to ₹1,50,000 |

| HRA Exemption | Not Available | Up to ₹1,92,000 (metro) |

| Section 80D (Health Ins.) | Not Available | Up to ₹25,000 |

| Home Loan Interest (Sec 24) | Not Available | Up to ₹2,00,000 |

| Net Taxable Income | ₹29,25,000 | ₹24,08,000 (approx) |

| Total Income Tax | ₹4,57,500 | ₹6,22,500 (approx) |

| Health & Education Cess (4%) | ₹18,300 | ₹24,900 |

| TOTAL TAX OUTGO | ₹4,75,800 | ₹6,47,400 |

| Monthly TDS (approx) | ₹39,650 | ₹53,950 |

| Tax Savings (New over Old) | ₹1,71,600 SAVED | – |

Key Insight: It saves ₹1,71,600 per annum compared to the Old Tax Regime at 30 LPA, unless you have an exorbitantly huge interest outgo on a very big home loan + full amounts under 80C + metro HRA + 80D together more than ₹5.17 lakh in total exemptions combined.

Read Also: 4.5 LPA In-Hand Salary: Monthly, Tax Deduction

Monthly In-Hand Salary Summary – 30 LPA

| Component | Monthly (₹) | Annual (₹) |

| Gross Monthly Salary (from employer) | 2,50,000 | 30,00,000 |

| Less: Employer PF (not in take-home) | -12,000 | -1,44,000 |

| Less: Gratuity (not paid monthly) | -4,810 | -57,720 |

| Gross Monthly Pay (received by employee) | 2,33,190 | 27,98,280 |

| Less: Employee PF Contribution | -12,000 | -1,44,000 |

| Less: Professional Tax | -200 | -2,400 |

| Less: Income Tax (TDS, New Regime) | -39,650 | -4,75,800 |

| NET IN-HAND SALARY (New Regime) | ~1,81,340 | ~21,76,080 |

| NET IN-HAND SALARY (Old Regime) | ~1,67,040 | ~20,04,480 |

Simplified: Monthly in-hand salary of 30 LPA In Hand Salary under the New Tax Regime is around ₹1,81,340. Under the New Tech Regime, where certifications and level of deductions are not too much, it comes down to close to ₹ 1,67,040 every month.

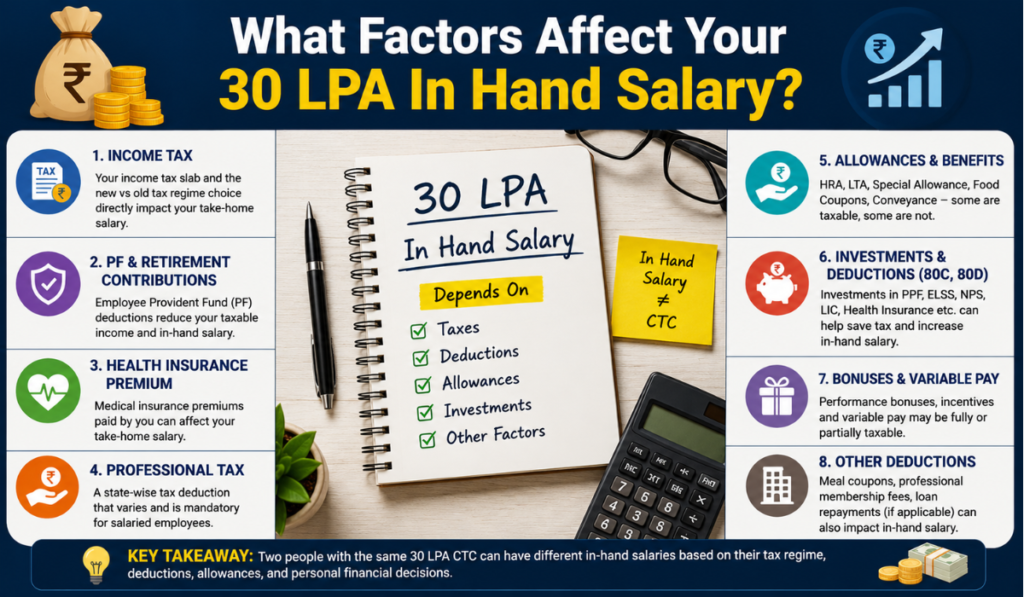

What Factors Affect Your 30 LPA In Hand Salary?

Tax Regime Selection

Between the New tax regime & Old tax regime, choose the right one for you (Biggest lever). For the salary of ₹30 LPA, the New Tax Regime has an annual saving of ₹1,71,600 for most salaried persons, but your unique condition, particularly house loan interests and HRA, could come down to this.

Basic Salary Percentage

Companies structure CTC differently. And as the Basic salary constitutes a larger chunk of the CTC (50% vs. 40%), this also means higher EPF contributions on both ends, which reduces monthly take-home pay but accumulates retirement savings faster. Lower Basic Salary = Less deduction on PF, which means more monthly in-hand but lower long-term savings.

Variable Pay and Bonuses

Several companies include an annual performance of 10–20% in the CTC. A ₹30 LPA split into ₹27–28 lakh fixed and ₹2.4–3 lakh variable means a lower take-home in the 1st month as you don’t get the bonus whatever it is so your fixed will be like ~₹1.6-1.7 lakh per month, plus probably given once or twice in the year and basically taxed on whichever month they decide to pay it out (probably when the books are closed).

Professional Tax

Professional tax varies by state. All states that you have mentioned will be ₹ 200/month (₹ 2,400/year) except the state of Maharashtra / West Bengal / Karnataka; a few states like Maharashtra, West Bengal, and KARNATAKA charge it differently. Some states have no professional tax at all.

City of Employment

Based on whether you live in a metro (Mumbai, Delhi, Bengaluru, Kolkata) and have to pay rent, you can also use HRA exemptions under the Old Tax Regime, which exponentially reduces your taxable income. As a result, the HRA exemption is not available under the New Tax Regime (a major consideration for employees living in metros with sky-high rents).

Gratuity and PF

Gratuity is deducted from your CTC (4.81% of Basic) but is not paid every month. You only take it as a one-time payment once you complete 5 years of continuous service. Likewise, due to the Employer PF contribution being within your CTC, it goes straight into your EPF account and is never a part of your bank.

30 LPA In Hand Salary: City-Wise Lifestyle and Savings

As for in hand salary, ₹1,81,000/month comfortably places you at the threshold that defines upper-middle class India if we consider a 30LPA. But, as far as this money goes, it wildly varies depending on where you live. Given below is an estimated breakup of expenses and possible savings in the larger Indian cities:

| City | Rent (2BHK, ₹/mo) | Monthly Expenses (₹) | Savings Possible (₹/mo) |

| Mumbai | 40,000–65,000 | 80,000–1,00,000 | 20,000–60,000 |

| Delhi / Gurugram | 25,000–45,000 | 65,000–85,000 | 50,000–90,000 |

| Bengaluru | 25,000–40,000 | 65,000–80,000 | 60,000–90,000 |

| Hyderabad | 18,000–30,000 | 55,000–70,000 | 75,000–1,00,000 |

| Pune | 15,000–28,000 | 50,000–65,000 | 80,000–1,05,000 |

| Chennai | 15,000–28,000 | 52,000–68,000 | 75,000–1,00,000 |

| Tier-2 Cities | 8,000–15,000 | 35,000–50,000 | 1,00,000–1,20,000 |

Stop it all, a 30 LPA In Hand Salary package actually gives you real financial security in any Indian city. The highest of these is even for the costliest of the metros, Mumbai, where you can save ₹20,000–60,000 a month comfortably after living both financially rich! At Hyderabad, Pune or Tier-2 cities, your savings could easily breach ₹1 lakh per month.

Read Also: 6 LPA In Hand Salary: Monthly Income, Deductions

Tax-Saving Strategies for 30 LPA Earners

Under the New Tax Regime

Standard Deduction (₹75,000): Automatically available. No investment or proof required. This means you can bring your taxable income down from ₹30,00,000 to ₹29,25,000 automatically and effortlessly.

NPS Employer Contribution: If your employer contributes to the National Pension System (NPS) on your behalf, this contribution (up to 10% of Basic) is exempt under the New Regime u/s 80CCD(2). This may relieve up to ₹1.20 lakh a year at a basic of ₹1.00 lakh/month, therefore making meaningful savings!

Meal Vouchers / Sodexo: Some employers provide meal vouchers, which are tax-free up to ₹2,200/month (₹26,400/year). Though small, these add up.

Under the Old Tax Regime

(₹1,50,000): Invest in PPF, ELSS MF, LIC premium or home loan principal repayment to avail maximum ₹ 1.5 lakh deduction. If you are living in a rented accommodation in a metro city, your HRA exemption can be high (around ₹ 1.5-2 lakh yearly) depending upon the lease paid.

Section 80D/ (₹25,000) This section allows a deduction for the amount of health insurance premiums paid by you or your spouse and dependent children up to 50 years. An extra ₹50,000 deduction is provided when parents are senior citizens.

Home Loan Interest (Section 24) – Interest on home loan for self-occupied property can be claimed as a deduction, up to ₹2,00,000 per year, one of the biggest deductions available for high earners.

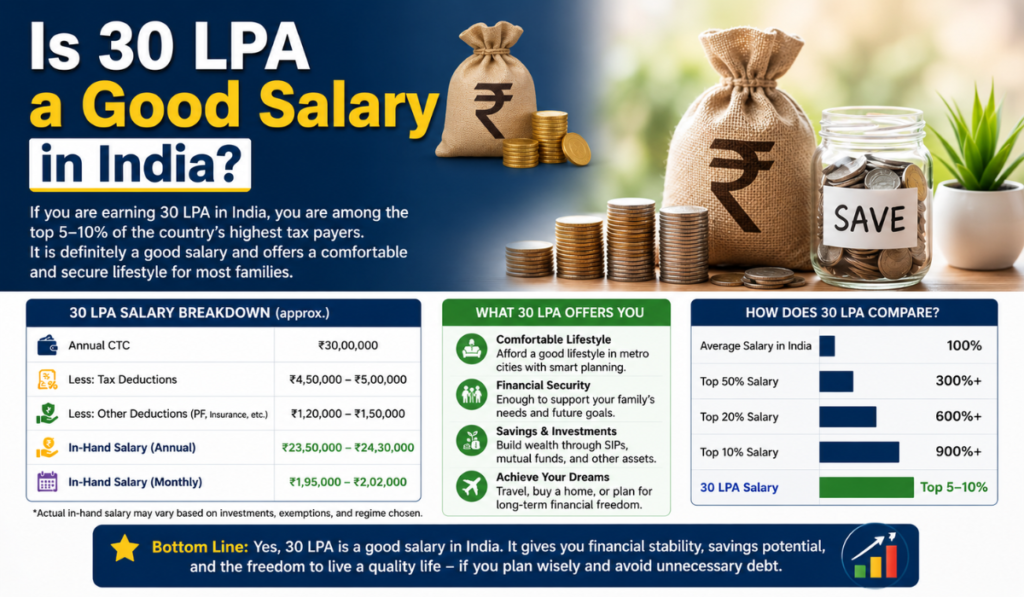

Is 30 LPA a Good Salary in India?

Yes, absolutely. With a 30 lakh per annum in hand salary, you would be in the top wage bracket of India. Data related to incomes provided evidence that most Indian salaried professionals earn less than ₹10 LPA. A ₹30 LPA CTC places you in the top 2–3% of income earners in this country.

₹1,81,000 in hand per month allows you a luxury lifestyle, rent a decent flat and drive your car, house, good schooling for kids (2-3), yearly vacations within the country or abroad; possibly ₹50,000–1,00,000 either saved or spent on luxuries depending on the city. If invested via SIPs into equity mutual funds systematically, this translates to a corpus of ₹1.5–2 crore in 10 years at conservative market returns.

That said, ‘good’ is relative. Forget the top 5 Indian cities; in smaller Indian cities or even towns, ₹30 LPA is tremendous prosperity. Comfort (not wealth) by Mumbaikar/Gurgaon standards (with rent, school fees, car EMI & lifestyle). As you can see, being sold a Bill of Goods with the whole “money management” fad does little good unless you’ve been trained to catch the fads before they harm you and are still engaged in intensive study, another sign of not having enough money at this level where intelligent tax planning with a combination of limited exemption asset protection during your lifetime should be leveraged into providing sufficient cash flow combined with prudent withdrawals from guaranteed investments that apply for elderly/retirement accounts.

Read Also: 7 LPA In Hand Salary: Monthly Salary, Deductions & Take Home Pay

Frequently Asked Questions (FAQ) – 30 LPA In Hand Salary

Q1. You have 30 LPA, how do you calculate the in-hand monthly salary for 2026?

New Tax Regime (FY 2026-27) Standard Salary Structure (40% Basic) In Hand Salary: ~30 LPA ₹1,81,000–₹1,84,000/month Limits to the Old Tax Regime with limited 6:1 Deductions appear only one single time, around ₹1,67,000–₹1,72.

Q2. How do you calculate the in-hand salary of 30 LPA?

Assuming CTC of ₹30,00,000 Gross Salary (₹27,98,280) = Gross salary + less Employer PF (₹1,44,000) + Gratuity (₹57,720). Then from the Gross Salary, subtract Employee PF (₹1,44,000), Professional Tax (₹2,400) and Income Tax( ₹4,75,800 under New Regime) to reach net in hand = ₹21,76,080 annually & ₹1,81,340 monthly.

Q3. Is the New tax regime better at 30 LPA?

A. In most cases, yes. New Tax Regime 30 LPA vs Old Regime vs ₹1,71,600 saved annually. The case for the Old Regime gets better only if you have a very high total of tax-free deductions, preferably a home loan with a big interest, full 80C investments, including VF investments, metro HRA and 80D that total more than ₹5.17 lakh together.

Q4. How to calculate income tax for 30 LPA?

Total income tax on ₹30 LPA Under New Tax Regime (FY 2026-27) ~₹4,75,800/Year (incl. If we consider the Old Tax Regime with enhanced basic deductions, that would be around ₹6,47,400. Monthly TDS in the New Regime comes around to ₹39,650.

Q5. Is 30 LPA gross or CTC?

(Usually, the 30 LPA refers to CTC (Cost to Company), meaning the total annual amount that your employer spends on you.) It covers base pay, HRA, allowances, employer PF (Provident Fund), gratuity, bonuses and insurance. Paay salary Insoorangeslls: Your gross and in-hand pay shall not exceed 30 LPA

Q6. Based on the above example, we can see that EPF / PF deduction is taken from 30 LPA.

The employee’s PF contribution is 12% of the basic salary. If the Basic is 40% of a 30 LPA package, then this means ₹1,00,000/month basic → Employee deduction of ₹12,000/month (or with other benefits or exemptions = ₹1,44,000/year). Your CTC also includes ₹ 12,000/month as an equal Employer PF contribution, but this one doesn’t hit your bank account.

Q7. After the announcement of significant tax reform, salaried employees will get a huge benefit in FY 2026-27 from the standard deduction.

As per the FY 2026-27 New Tax Regime, the standard deduction allowed to salaried employees increased from ₹50,000 in the previous year to ₹75,000 per annum. It is automatic, reduces your taxable income without having to do any investing or paperwork.

Q8. The example is for illustration of the budgeting process. DSC, can you save Rs 1 lakh from ₹30 LPA?

Indeed, it’s quite real, particularly for anyone living away from the priciest metros. Why live a life in cities such as Hyderabad, Pune, Chennai or other Tier-2 cities, you can manage your monthly expenses within ₹60,000–80,000, and, like some people, put aside 1 Lakh+ per month for savings and investments. Well-disciplined savers in either Bengaluru or Delhi can exceed ₹80,000–90,000 per month.

Q9. What is the net take-home salary if Variable Pay is included within the 30 LPA?

If your fixed monthly in-hand is roughly ₹1,50,000–₹1,60,000/month on the fixed components and 10–15% of this 30 LPA is a variable (near ₹3–4.5 lakh) to be paid quarterly or annually. The variable compensation is taxed in the month it is paid.

Q10. Best Investments for Someone Earning 30 LPA in India?

Investors with annual incomes of 30 LPA can be advised to invest ₹30,000–50,000/month in SIPs in equity mutual funds for wealth created over a long time frame; NPS for retirement + benefit u/s Section 80CCD(2), PPF because it is risk-free compounding; term insurance (1 crore + cover); family health insurance; home loan if applicable since this can serve the dual purpose of HRA replacement plus Section 24 deduction on interest paid*.

Conclusion: 30 LPA In Hand Salary

There is more to your in hand 30 LPA, it is about taking the right decisions on tax planning, investments and budgeting + Financial Goals. A headline CTC of ₹30,00,000 leads to an absolute monthly take-home of around ₹1,81,340 under the New Tax Regime, higher than mine by about a tad (the rest being consumed by income tax, PF contribution, gratuity provisioning and professional tax ).

The New Tax Regime is obviously the better option for nearly all 30 LPA earners in FY 2026-27, with an annual tax savings of almost ₹1.72 lakh over the Old Regime. But if you have a high home loan, metro rent and aggressively invest in 80C instruments, both the regime calculations should still be run before taking a decision.

In India, ₹30 LPA puts you into a high-income tax system, but with smart input along with the right regime choice & some disciplined investing, this can be the base of true long-lasting wealth. You know your 30 LPA in hand salary number, work around it and make every rupee count.

Yashika is the dedicated content writer and salary research author at TheMonthlySalary.com. She specializes in creating clear, helpful, and easy-to-understand content about monthly salary, in-hand pay, salary calculators, career growth, and salary updates. Her goal is to simplify salary-related topics for employees, job seekers, students, and working professionals. Through well-researched guides and practical insights, Yashika helps readers make smarter career and financial decisions.